You’re inundated with a deluge of articles and guidance emphasizing the urgency of transferring your assets out of your estate now. Your failure to do so might result in significant tax liabilities.

The U.S. government has introduced an unprecedented historical gift tax exemption, allowing individuals to gift assets up to $12.92 million individually or jointly with their spouse, totaling $25.84 million. This exemption amount increases annually in line with the Chained Consumer Price Index.

However, this exceptionally high exemption is set to expire in 2025, after which it will decrease to an estimated range of $6 million to $8 million, depending on factors such as inflation.

You’ve likely read this estate tax exemption is a point of contention between Democrats and Republicans. Democrats aim to eliminate it, while Republicans seek to extend it. This perpetual political battle adds another layer of uncertainty.

What does all of this mean for you? It’s nearly impossible to provide an exact answer, so I’ve devised a hypothetical scenario to illustrate the potential impact.

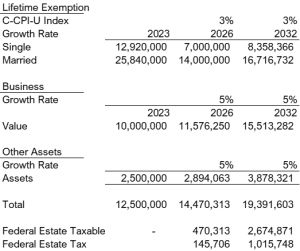

Suppose your business is presently valued at $10 million, and your other assets (investments, residences, etc.) amount to around $2.5 million, with both appreciating by 5% annually. This example assumes you are married and have not utilized any of your lifetime exemption. The scenario calculates potential taxes at the later of your and your spouse’s date of passing. Current federal regulations allow for the tax-free transfer of assets between spouses. Estate taxes may apply if assets are bequeathed to children or other beneficiaries upon your demise.

Note that this example does not consider state estate taxes, because they vary widely. Some states do not acknowledge gifts, while others impose no estate taxes at all. Additionally, some states may not permit a spousal exemption, making it essential to consult your professional advisors for tailored guidance.

Let’s explore the potential tax consequences of this scenario. I’ve ended the projection in 2032 simply as a placeholder. The longer you and your spouse live, the greater the potential estate tax liabilities. The tax rates utilized are current as of 2023 and are subject to change.

Gifting assets does not need to lead to a reduction in your income. Your professional advisor is best equipped to devise a plan that preserves your income while addressing these tax considerations.

Imagine you and your partner formed an electrical contracting company. You, Operations Partner, handle operations, Marketing Partner handles marketing and admin. It’s a beautiful arrangement. It has worked well for decades.

Their Attorney tells them “You need a funded buy sell agreement. If one of you dies, how will the company move on?”

“Another legal document? Another fee? And life insurance premiums, too? All money we can invest in the business or pay to ourselves!,” you exclaim!

A big takeaway from COVID is the unexpected will happen and always at the worst time. Avoiding the future is as impossible as living forever. The future happens whether we are ready for it or not.

Marketing Partner tragically dies. Their spouse is distraught. Operations Partner now has a new partner, Marketing Partner’s Spouse. Spouse knows nothing about electrical contracting and has zero interest in being involved in the business.

Operations Partner now runs the business alone. S/he is fielding calls from the Marketing Spouse and Spouse’s professional representatives. “Where is my money? How can I live with no income? You must help me!”

A well-written life insurance funded buy sell agreement will lay out what happens when a partner passes. It avoids these difficult circumstances and can fund a buyout.

What is the smart solution to avoid stress and costs?

Invest in an insurance buy-sell agreement.

Please consult with your CPA and attorney to see the implications for you.

Those of us working in the trusts and estates area see the strain when mom or dad dies, and no estate plan is in place. Siblings often go to war. Holidays and other celebrations will never be the same. Long-held resentments resurface. Even if mom or dad is very sick or dying when estate planning is brought up, we hear, “Mom always liked you better!” or “Eileen always took my teddy bear away.” Our simple response, “Oh, just grow up!” can only be said in our heads.

While planning an estate’s distribution is always difficult, business owners face an especially tricky situation – “How can I be fair to everyone when my biggest asset is my business?” As with many decisions when family is involved, the question is seen as overwhelming. This essential planning never starts.

Being fair is relatively straightforward when the assets are cash, investments, and homes. Appraise the house, add the investments and the cash, split the total among the heirs. When a business is involved, the definition of fair becomes nebulous. Consider the following example, business owner Mr. X has one operating business and one real estate company whose only tenant is the business. Mr. X has one daughter who is a key employee in the business and is slated to take over when Mr. X passes away. Mr. X’s two sons, however, do not work in the business. How can Mr. X divide the estate fairly? Let’s assume the daughter is not paid market compensation. Few small businesses pay market rate salaries to their family employees. Let’s also assume market rent is not paid. Rent paid to related companies usually is just enough to cover mortgage payments, real estate taxes and other miscellaneous costs.

Solution 1: Leave the building to the two sons and the business to the daughter. Make up differences with cash, investments, or insurance.

As the building’s owners, the two sons deserve market rent. But imposing market rent on the daughter may adversely affect the business’ profits and her income.

Without control over the building, the daughter may feel at risk. Barring a formal and very long-term lease, the two sons can sell the property and leave the daughter’s business homeless.

The business may falter or even fail through no fault of the daughter. COVID provides innumerable examples of this. The daughter now owns a company that is worth less or is even worthless. the two sons still hold a valuable building.

Solution 2: Evenly divide the ownership of both companies among all three children.

The daughter may resent putting in the sweat equity required to increase profits – profits the two sons share though they have not lifted a finger.

The two sons may want the daughter’s salary to be at market rates. While the business may show more profits, the daughter may now be taking a pay cut.

There are three sibling-owners. As children the siblings could never agree on the restaurant the family should go to for dinner. Can the business owner expect them to agree in the future on important issues?

Solution 3: Sell the business to an Employee Stock Ownership Plan (“ESOP”) and divide the proceeds among all three children. An ESOP may be the right solution for the right company.

In short, an ESOP is a trust that purchases stock from the owner(s) on behalf of the company’s employees as a retirement benefit. The ESOP must comply with various federal (and sometimes state) regulations including annual filings. It is subject to audit/review by the IRS and the Department of Labor.

As a trust, it is tax exempt, providing more cash flow to the company. Contributions to the ESOP are tax deductible, even principal payments on loans taken to finance the share purchase. Limits to these benefits exist.

Among the pros and cons of an ESOP are:

Pros

An ESOP is typically income tax exempt, company cash flow is improved.

ESOPs can be financed at lower interest rates and loan repayments can be tax deductible.

The sale can be accomplished over time.

The owner/seller can realize potential tax deferral benefits.

Employee morale often rises.

Cons

The Company must produce strong and consistent cash flow.

There are expenses to set it up, often well over $50,000 plus.

There are annual expenses for filings, valuations and if the plan is large enough, audits.

There is risk of audit by the IRS and the Department of Labor (“DOL”). An unhappy or disgruntled employee can lead to an audit by the DOL.

A trustee must be engaged. While often the trustee is not involved in day-to-day decisions, they are entitled to ask questions.

These few but typical issues certainly should not stop a business owner from planning. They often do, however, there are always alternatives. As hard as family conversations about the estate’s division are guaranteed to be, they must occur. Without them, the minor fights that may occur are nothing in comparison to the guaranteed chaos that will follow the owner’s demise.

The results from our very unscientific LinkedIn survey are in, and the results are, well, mixed. Our goal was to see how effective LinkedIn, probably the largest professional network worldwide, is for our clients and referral sources. Of the respondents, about 1/3 provided professional services, another 20% were distributors while 25% offered services to consumers. The balance was in a variety of professions.

Over half of the participants review LinkedIn 2-3 times a week, another quarter look daily while the rest rarely look. When asked if this was the same as three year ago, about half said they look more today, a quarter said less while the balance indicated it was the same.

Only 10% advertised on LinkedIn but all deemed it only somewhat effective.

So, what do they use LinkedIn for, I asked? While many looked for clients and employees through LinkedIn, keeping track of colleagues and competitors was by far the most important response.

Of those few that quit LinkedIn, it was either not effective for them or too time consuming.

What did I conclude?

LinkedIn continues to be a source of information many of us use. While sometimes my own landing page seems to hold more advertisements than information, I am guilty of indulging a few times a week.

Guest Feature by Ben Golden, Certified Tax Planner and Certified Tax Coach

Imagine you have a hidden treasure, buried right beneath your feet. You’re busy tending to your flourishing business garden, watering the plants, checking the soil, and soaking up the sunshine, unaware that you’re standing on a goldmine. This is what personal goodwill is like in the world of business.

So, what is this personal goodwill we’re talking about?

The world of business is an adventure. In every adventure, there’s a treasure waiting to be discovered. In the journey of a business owner, there’s a secret goldmine that’s often overlooked – personal goodwill. Like a hidden treasure chest, personal goodwill could become your secret weapon in tax planning, saving you a significant fortune when you decide to sell your business.

Now, you might be wondering, what is this invisible goldmine? Personal goodwill is like the charm of your favorite superhero, their charisma that draws people to them. It’s the relationships, reputation, skill sets, and the personal know-how that you, as a business owner, bring to your company. Think about that loyal customer who follows you no matter where you go, or that supplier who gives you priority because they like doing business with you. These are all components of your personal goodwill.

While this sounds like an enticing opportunity, it’s important to remember that leveraging personal goodwill comes with its own set of challenges. The first hurdle, as illuminated by the Bross Tax Court decision (Bross Trucking Inc., T.C. Memo 2014-107), is to establish that personal goodwill exists separately from corporate goodwill. This is a bit like proving that you have two superheroes in your team, each with their own distinct abilities. Personal goodwill, your superhero, is your reputation, your relationships, and your unique business acumen. However, the challenge is to show that these two superheroes are not one and the same. It requires evidence that your personal attributes and relationships are directly responsible for your business’s success, and not merely the business’s brand or products.

The second hurdle is making sure that your superhero isn’t tied down to your business. This means proving that you, as a business owner, have the right to sell your superhero’s services separately from the rest of your business. If you’ve signed an employment contract or a non-compete agreement that ties your superhero down to your business, it means that you can’t sell your superhero’s services separately from your business. So, to navigate this challenge, you need to show that no such contractual agreements exist.

Now, let’s imagine how this works in the real world. Say you’re selling your business. Typically, the sale price is subject to double taxation – once at the corporate level and then at the shareholder level when the proceeds are distributed. But here’s where your superhero, personal goodwill, swoops in to save the day. When a part of the sale price is allocated to your personal goodwill, that portion is taxed only once at the individual level, typically at a lower capital gains tax rate. This could result in significant tax savings, making the process of selling your business more beneficial for you.

The adventure of personal goodwill, while filled with potential pitfalls and challenges, also carries the promise of a treasure trove of tax savings. With careful planning, astute understanding, and the guidance of a trusted tax advisor, you could navigate these challenges and unlock the hidden goldmine of personal goodwill. So, gear up, business owners. It’s time to harness your personal goodwill superhero and make your business selling journey a victorious adventure!

Ben Golden is a Certified Tax Planner and Certified Tax Coach with offices in the Chicagoland area and Alabama. He has two sister companies (Golden Tax Relief LLC and IRS Trouble Solvers) that he manages. Ranked among the Top 10 Tax Resolution Experts in the country, Ben Golden’s company, IRS Trouble Solvers LLC., focuses on Resolution. However, Ben’s tax planning company, Golden Tax Relief LLC also reached national notoriety by being in the top 500 fastest growing companies in the nation (Inc. 5000) last year… Ben earned his BS in Accounting from The University of Alabama in 1999, followed by an MS in Taxation from Golden Gate University in 2002. Ben is an Enrolled Agent, the highest designation provided by the Internal Revenue Service! Along with actively participating in his multiple businesses, Ben is also a member of the American Society of Tax Problem Solvers (ASTPS), American Institute of Certified Tax Planners (AICTP), President of Alabama Society of Enrolled Agents (ALSEA), member of National Association of Enrolled Agents (NAEA), National Society of Accountants (NSA), Tax Representative Network (TRN), National Tax Practice Institute Fellows (NTPI), is a Coach with Corvee, and is in several Mastermind groups.

Ben Golden is a Certified Tax Planner and Certified Tax Coach with offices in the Chicagoland area and Alabama. He has two sister companies (Golden Tax Relief LLC and IRS Trouble Solvers) that he manages. Ranked among the Top 10 Tax Resolution Experts in the country, Ben Golden’s company, IRS Trouble Solvers LLC., focuses on Resolution. However, Ben’s tax planning company, Golden Tax Relief LLC also reached national notoriety by being in the top 500 fastest growing companies in the nation (Inc. 5000) last year… Ben earned his BS in Accounting from The University of Alabama in 1999, followed by an MS in Taxation from Golden Gate University in 2002. Ben is an Enrolled Agent, the highest designation provided by the Internal Revenue Service! Along with actively participating in his multiple businesses, Ben is also a member of the American Society of Tax Problem Solvers (ASTPS), American Institute of Certified Tax Planners (AICTP), President of Alabama Society of Enrolled Agents (ALSEA), member of National Association of Enrolled Agents (NAEA), National Society of Accountants (NSA), Tax Representative Network (TRN), National Tax Practice Institute Fellows (NTPI), is a Coach with Corvee, and is in several Mastermind groups.

Ben Golden is a Certified Tax Planner and Certified Tax Coach with offices in the Chicagoland area and Alabama. He has two sister companies (Golden Tax Relief LLC and IRS Trouble Solvers) that he manages. Ranked among the Top 10 Tax Resolution Experts in the country, Ben Golden’s company, IRS Trouble Solvers LLC., focuses on Resolution. However, Ben’s tax planning company, Golden Tax Relief LLC also reached national notoriety by being in the top 500 fastest growing companies in the nation (Inc. 5000) last year… Ben earned his BS in Accounting from The University of Alabama in 1999, followed by an MS in Taxation from Golden Gate University in 2002. Ben is an Enrolled Agent, the highest designation provided by the Internal Revenue Service! Along with actively participating in his multiple businesses, Ben is also a member of the American Society of Tax Problem Solvers (ASTPS), American Institute of Certified Tax Planners (AICTP), President of Alabama Society of Enrolled Agents (ALSEA), member of National Association of Enrolled Agents (NAEA), National Society of Accountants (NSA), Tax Representative Network (TRN), National Tax Practice Institute Fellows (NTPI), is a Coach with Corvee, and is in several Mastermind groups.